DMASS Europe’s chairman, Hermann Reiter, was keen to stress there is no cause for alarm, saying that this market consolidation was long overdue. “Everyone should have prepared to weather a few quarters of weak bookings and billings,” he said, adding “It does not make sense to over-react with cost-cutting now, when there is a huge potential for recovery across all industry segments and technologies. Electronic components will remain the key technology for innovation and transformation for many years to come.”

DMASS Europe’s chairman, Hermann Reiter, was keen to stress there is no cause for alarm, saying that this market consolidation was long overdue. “Everyone should have prepared to weather a few quarters of weak bookings and billings,” he said, adding “It does not make sense to over-react with cost-cutting now, when there is a huge potential for recovery across all industry segments and technologies. Electronic components will remain the key technology for innovation and transformation for many years to come.”

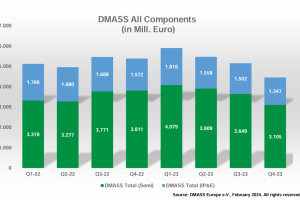

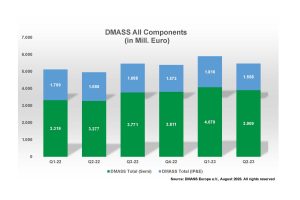

After three years of “significant growth” Q1 2024 showed a decline of more than 23% across all components and is seen to portend “a few challenging quarters,” said DMASS. Members reported consolidated distribution revenue declines of 23,3% to €4.58bn, with semiconductors dropping by 26.5% to €3bn and IP&E (interconnect, passive and electromechanical) components lower by 16.3% to €1.57bn.

The UK proved to be the most resilient in the semiconductor sector with just a 15% decline, followed by Italy (down 19.88%) with Germany experiencing -30.26%, Benelux declining 35.86% and Switzerland and Nordic and Austria experiencing the largest declines in Q1 (-35.49%, -32.27% and -40.20% respectively).

Reiter was sanguine, describing Q1 2024 as “the least surprising quarter I have seen in a while. Even if we may face a few challenges over the next few quarters, recovery will start sooner or later, and I am confident that 2025 will be back on track,” he said. “It wouldn’t make sense to overreact now with cost-cutting exercises. The multiple crises the world is facing right now should hide the simple truth that the electronics revolution is ongoing: from the all-electric society to artificial intelligence, the world needs more and more innovative components. We will find more opportunities than resources to realise them.”

Across all countries, only high-power LEDs and microprocessors showed growth, with discrete semiconductors declining 30%, power semiconductors declining 20.55%, sensors and actuators (-31.29%), optos (-18.06%), analogue (-31.09%), memory (-19.88%), MOS micro logic (-23.32%), programmable logic (-36.65%) standard logic (-31.60%) and other logic declining by 24.46%.

IPE also declined in Q1, by 16.3% to €1.57bn, with passives hardest hit at -21.18%, then electromechanical (-13.10%) and power supplies (-13.36%). DMASS also reported that central Europe (Germany, Austria and Switzerland) suffered most (-23.24%, -27.89% and -20.57% respectively) and UK, France, Italy and Iberia did “surprisingly ok” (-12.49%, -12.82%, 11.23% and -10.15% respectively).

Chairman Hermann Reiter concludes: “It is becoming increasingly clear that the components market is much more complex than what you may see in global market predictions. For example, the AI hype is not happening everywhere and only involves a few component types”.