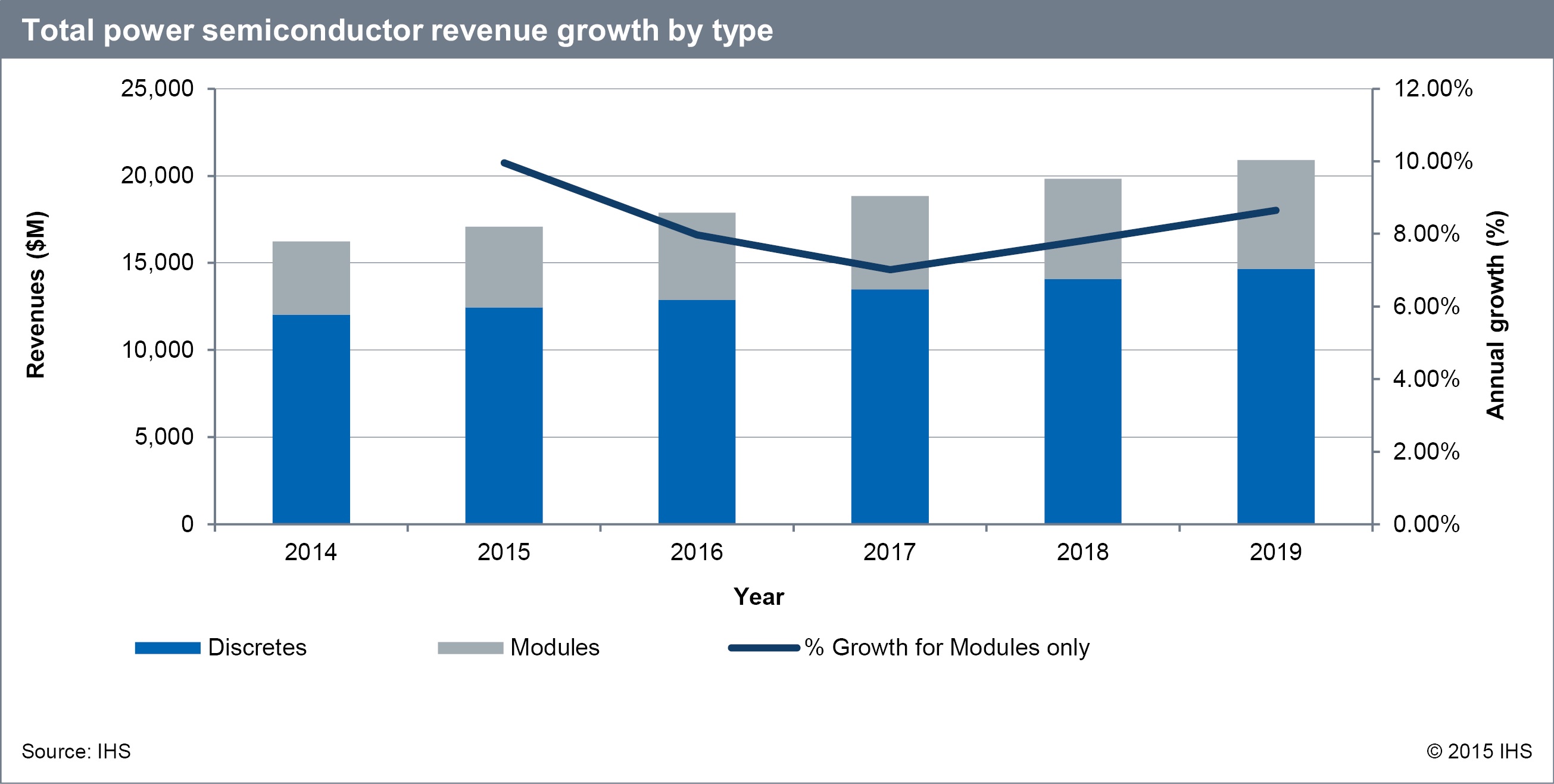

In 2014, y-o-y power discrete revenue grew 5% and power module revenue grew 12%.

The global power module market is projected to comprise nearly one third (30 percent) of the power semiconductor market by 2019, growing at twice the rate of power discretes, from 2014 to 2019, says IHS.

“OEMs will continue to want modular power solutions, which can be integrated easily into various subsystems and used in many different devices,” says IHS’ Richard Eden, “power modules are widely found in inverters for wind converters, photovoltaic solar energy systems and other renewable energy applications. They are also found in industrial motor drives and hybrid and electric vehicles.”

Infineon continued to be the largest supplier for the global power semiconductor market in 2014, with an estimated market share of 13%. Mitsubishi ranked second, at 7%. ST moved up to the third market position, displacing Toshiba, with an estimated market share of 6%.

With the acquisition of IR by Infineon last year, the market landscape for power semiconductors is changing. The merged companies held almost 27% of the power transistor market in 2014.

The transistor product category includes bipolar transistors, metal-oxide semiconductor field-effect transistors (MOSFETs), and insulated-gate bipolar transistor (IGBT) products, accounting for about two thirds of the total discrete power semiconductor market.

Mitsubishi Electric was the largest supplier for power modules in 2014, although the company’s estimated share of the market remained at 24% for 2013 and 2014. Infineon maintained the second-ranked position at 20%.

The top four power module suppliers – Mitsubishi, Infineon, Semikron and Fuji Electric – accounted for 65% of the global power module market in 2014.