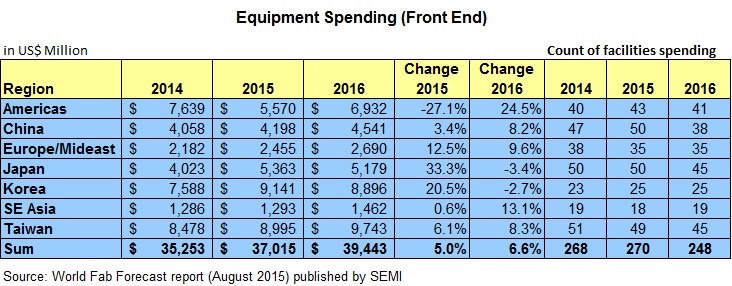

SEMI data indicates that some companies still plan to increase equipment spending in the second half of 2015, compared to the first half.

Foundry is expected to slow in 2015 (-3%) but is expected to gain momentum in 2016 (14%).

In memory, equipment spending is predicted to grow 16% by the end of 2015, but will drop about 1% in 2016.

Mirroring slow growth in capex and equipment spending, growth in worldwide installed capacity growth is forecasted at between 2 and 3% in both 2015 and 2016.

The most added capacity will be seen in foundries (5% in 2015 and 4% in 2016), Flash including 3D NAND (5% in 2015 and 3-4 %in 2016), and LEDs (14% in 2015 and 9% in 2016).

Capacity additions vary by wafer size, with slow steady gains in 200mm wafers while 300mm capacity may grow less in 2016. . Capacity additions vary by wafer size with increasing gains in 200mm wafers from 1.6% in 2015 to 2.4% in 2016 and continuous growth for 300mm wafers with 4 % each in 2015 and 2016.

At least 23 facilities (with various probabilities) will begin construction in 4Q15 or later in the future. In 2015, SEMI forecasts 17 new construction projects and in 2016, SEMI expects 11 new construction projects.

SEMI tracks a total of 43 new and continuous construction projects in 2015 with investment totalling over $5.9 billion.