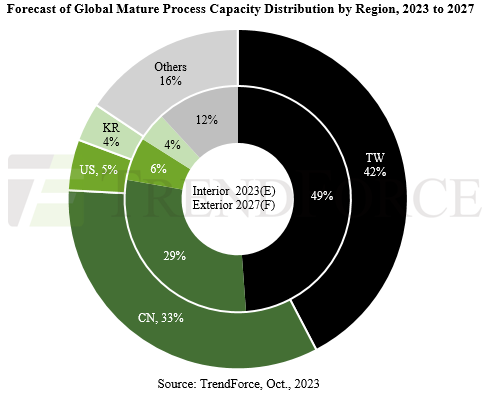

The result could be a price war in mature process products and increasing localisation for driver ICs, CMOS image sensors, and power discretes.

Leading China’s charge are: SMIC, HuaHong and Nexchip:

SMIC’s 28HV and Nexchip’s 40HV are gearing up for mass production in 4Q23 and 1H24 respectively;

SMIC and Nexchip are ramping up CMOS image sensor processes in the 45/40nm and 50/55nm ranges;

Grace, SMIC, Nexchip, CanSemi, GTA and CRMicro are expanding capacity for power discretes like IGBTs and MOSFETs.